Insurance companies have long provided policies to cover losses of property but, before the end of the Civil War, this also included pay-outs for injury and death of the formerly enslaved. This slavery-era business precaution is not only a vivid example of the objectification of people as property, but it also shows that both sides of the Mason-Dixon Line profited from slavery, since many of these insurance companies were from the north.

In 2000, the California Senate approved a bill (SB 2199) that required insurance companies currently doing business within California to submit any pre-1865 slave insurance policies they or their former corporate incarnations had issued. In 2002, the California Department of Insurance (CDI) reported that of the 1,357 companies who met the requirements and had been contacted, 92% had responded.

Of those who responded, the vast majority reported they had not been in business until after 1865. Of the companies that had operated before 1865, many reported their archival investigations had not turned up any slave policies—not necessarily because they had not been involved in the practice, but oftentimes because the company policies had been to destroy documents beyond a certain age.

However, some insurance companies had been able to find and submit copies of original slavery era policies to the CDI. Aetna Life Insurance Company, AIG, Manhattan Life, New York Life, and Royal & Sun Alliance are among those who provided these documents or limited evidence that policies may have been issued.

The copies submitted to CDI cover approximately 400 slave owners for approximately 600 slaves, most of these issued by Nautilus Insurance Company, operating out of New York (now New York Life). These policies usually contain the first name of the slave (sometimes with the surname of the owner), the owner’s name and location, the premium and insured value and, sometimes, the occupation of the slave.

So why is the genealogy librarian writing about this?

Solid information about our slave ancestors is notoriously hard to locate. Largely because before the 1870 U.S. federal census, slaves were only identified by gender and age, not by name. Because of this, a person has to get creative in identifying resources that might shed light.

Slavery-era probate records (wills) and post-slavery bank and employment contracts (The Freedman’s Bureau) are good resources to try. But other bodies of data that were established for reasons not even remotely tied to genealogical research (like these insurance policies) have interesting genealogical potential.

Although these policies usually only identify the first name of the slave, they may be helpful in tying a specific person to a specific slaveholder in a specific location at a specific time. This might allow you to connect the dots between that all-important 1870 census and where your slave ancestors were before.

The policies themselves are not yet available online, but I’ve talked with the Family History Library and they are interested in digitizing them. I’ve also spoken with Leslie Tick, the current Policy Approval Bureau Chief-Assistant Chief Counsel at the CDI. She was also the Senior Chief Counsel and point-of-contact at the CDI when this bill was approved, and she told me the only reason they didn’t digitize the actual documents at the time was because they didn’t have the resources nor technology to do so. But she emphasized the intention is to make these documents available for all to see, and she was very positive about the idea of digitization.

However, in 2002, the CDI distributed physical copies of the insurance policies to several public repositories—the Los Angeles Public Library being one such recipient. The documents are held in a large box at the Social Science, Philosophy and Religion Department's Reference Desk, which you can access if you provide I.D. The box contains letters of response from the insurance companies, copies and commentary about the Senate bill, and printed copies of an index to the policies. Then, of course, you’ll find copies of the policies. Full disclosure: they are hand-written, poor copies (from fragile originals), and hard to read. If the policy you’re looking for was provided by New York Life/Nautilus, the record number on CDI’s index will correspond numerically with their order in the box.

The online index is a good place to start. There are two versions: one sorted by slave name; the other by slave owner. The indexes are also annotated with most of the information from the policies. Here’s an example:

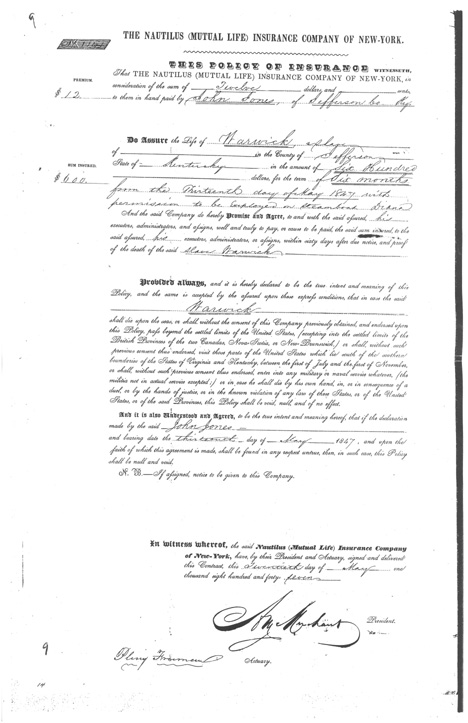

This index record tells us the policy was submitted to CDI by New York Life and is for a slave named Warwick of Jefferson County, Kentucky. The slave owner is John Jones of the same location. We also learn the policy number, date of Warwick’s death, and that he was employed as a fireman on the steamboat “Diane.”

When looking at the three physical documents to which this index record points, we learn a little more information. The first two documents are the original policy and the receipt of payment.

The extra information we get—that was not included in the annotated index—is the premium amount ($12), the amount of insurance ($600), the life of the policy (6 months from May 13, 1847), the date of the policy (May 20, 1847), and we see the signatures of the President and Actuary of Nautilus Insurance (although it’s hard to decipher their names).

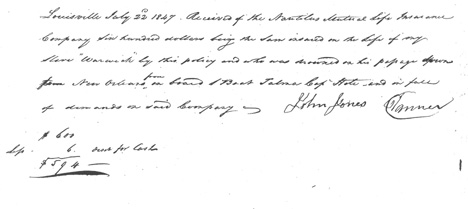

The third policy document is a receipt dated July 22, 1847, signed by John Jones, saying he had been paid $600 by Nautilus because Warwick drowned during passage on the steamboat “Talma” from New Orleans.

John Jones paid Nautilus Insurance Company a premium of $12 in 1847, and was paid $600 when his slave Warwick died. In today’s terms, that would be approximately a $350 premium on a policy which paid $17,800.

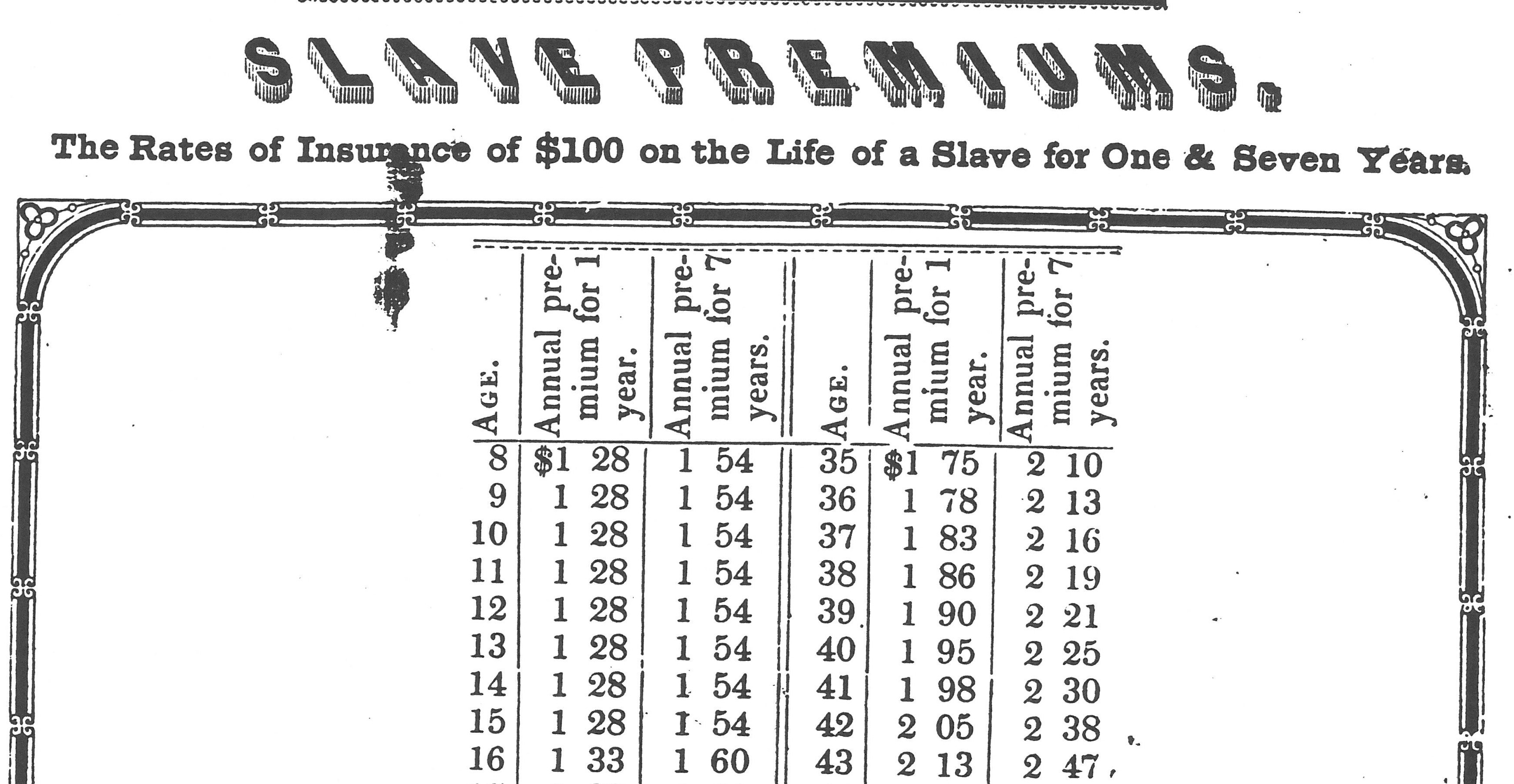

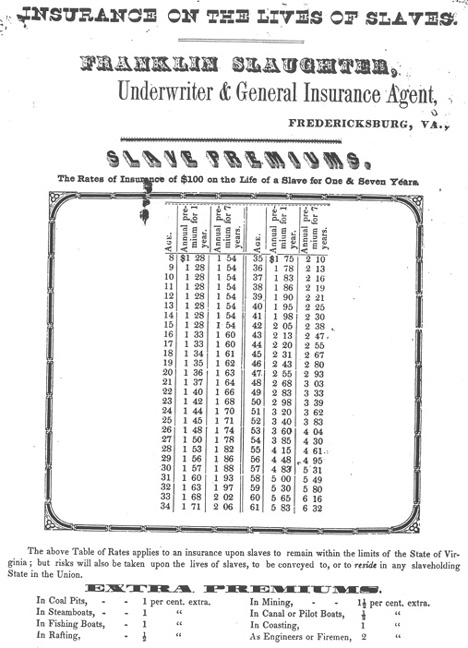

Another interesting document provided to CDI was a table of insurance rates for slaves in Virginia. It had been provided to them by Penn Mutual, but this insurance company had not issued any slave insurance policies—before the end of the Civil War, they had only been licensed to do business in Pennsylvania, which was not a slave state. It was mysterious how it turned up in their archives, but they submitted it in the spirit of full disclosure.

Other states have followed California’s lead in passing legislation to require companies that had once profited from the slave trade to come forward. The Illinois Department of Insurance has a similar insurance-policy index online.

And there are other forms of slave-business activity that cities are trying to ferret out before hiring contractors, like Oakland’s “Slavery Era Disclosure Ordinance." This is an ordinance “requiring city contractors who provide insurance, financial, and other services to the city to research and disclose to the city records evidencing benefits from the American slave trade.” Besides banks and insurance companies, other industries who have to come clean per this ordinance are textile, tobacco, railroad, shipping, rice, and sugar companies. Whether the documents these companies find in their archives will have genealogical value remains to be seen (i.e. will they list individuals by name?).

If we can find something useful in the archives of our terrible slave-era past to help us fill in the lives of our enslaved ancestors, it may be a way to turn the original intent of those materials on its ear. I had first read an article about these slave insurance policies in The Baobab Tree, the newsletter of the African American Genealogical and Historical Society of Northern California, and thought it had been so imaginative to sort of “repurpose” these documents for genealogical value.